Financial Plans To Take Up For A Young Family

Assuming you have followed my advice from my previous article, you and your spouse’s insurance coverage needs should be well taken care of. Now, it is time to start planning for your child.

Financial planning for a child would always start with a Hospitalisation & Surgical plan (a.k.a. Health Insurance), just like any adult. For more information on what to look out for in a health insurance, you can read my in-depth article in the Apr / May issue of The New Age Parents e-magazine.

Financial planning for a child would always start with a Hospitalisation & Surgical plan (a.k.a. Health Insurance), just like any adult. For more information on what to look out for in a health insurance, you can read my in-depth article in the Apr / May issue of The New Age Parents e-magazine.

After the above is taken care of, you may start planning for your child’s tertiary Education Fund. Some financial planners advocate taking up a life insurance coverage for a child before planning for their tertiary education fund. Unless there are special circumstances to buy a life insurance plan for your child first, I would advocate planning for your child’s tertiary education fund because it is more time sensitive as compared to life insurance coverage. Your child would have to go for his tertiary education at 19 years old (if your child is a girl) or 21 years old (a boy). The longer the delay in planning for their tertiary education fund, the cost of savings will go up exponentially, due to the nature of compounded interest and returns.

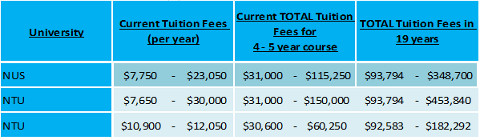

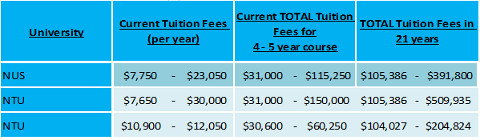

When I entered tertiary education 15 years ago, it costs me S$5,500 per year for a non-lab course. So how much does it cost to go to a university these days?

Hence, based on a quick calculation, the fees in our local universities have increased by a compounded rate of 2.31% per year. Do note that in certain years, the education providers did not increase the tuition fees due to Singapore’s economic conditions. But when there is an increase, it normally ranges between 4% to 6%.

Being a kiasu Singaporean and conservative financial planner, I always plan for myself and my clients using the 6% compound interest rate. Better to have more money later rather than have to tell my kid and client that they have to stop school while I save up more for their education fee.

With a new born, this is the lump sum amount you should save up when they are ready for local universities.

If your child is a girl (like in my case),

If your child is a boy,

Do note that I did not include education living costs (buying textbooks, photocopying fees, meals in schools, transportation, club and society fees are a few examples), because these amounts normally would not be more than S$600 per month. You could either help your child pay for these miscellaneous costs then, or they could find a part time / holiday job (as in my case) or you could also include this cost in your Education Fund planning.

I also did not include dormitory fees as this is, well, optional. Not all students stay in dorms and Singapore’s transportation system will only get better in future. However, feel free to inform your financial planner to include this cost in your Education Fund planning.

Thus far, I have only shared about future costs in local universities, how about costs in overseas universities? As there are many universities abroad, operating on different fee structures and many other factors to consider while abroad, I would not share these concerns extensively in this article. However, if you would like to know more, do drop me an email.

So what are some of the strategies you may use to help you achieve the above goal?

What are the financial instruments that can help you achieve your above goal?

You may consider the following:

- Endowment Plan (a.k.a Saving Plan)

– Plans that mature after a fixed period of time.

– Bonuses are added to this plan every year.

– There are now plans that allow you to save for a shorter period of time, rather than for the whole tenure of the endowment plan.

– There are also plans that pay out the Education Fund in 3 or 4 yearly instalments, earning you more interest.

- Anticipated Endowment Plan

– Plans that mature after a fixed period of time.

– Bonuses are added to this plan every year.

– Added flexibility of yearly cashback option. You may choose to take out this cashback for liquidity purpose or reinvest back into the endowment plan.

– Reinvesting would be a better option due to the power of compound interest.

– You should not be taking out monies from this plan before your child is ready to go to university anyway.

– However, this type of plan is normally more expensive compared to a normal Endowment plan due to the added flexibility.

- Investment-Linked Plan (ILP)

– Plans that have no fixed term.

– Able to withdraw cash anytime.

– Potentially higher returns over the long term.

– Subjected to investment risks.

– Needs continual monitoring in order to maximise your returns.

Professionally, I have never advised my clients to use Investment-Linked plans for their child’s Education Fund planning, because there are too much inherent risks and uncertainty involve (unless my clients insist on this plan, but so far so good). What if the market is not doing well when the child is ready for university? I do not think it would be nice for a client or child to hear, “Can you delay your education for a few years till the market is doing better?”

Hence, my advice would always be to go for either endowment plans or anticipated endowment plans. As I have mentioned, I am a kiasu Singaporean and conservative financial planner.

Have any ideas to share or need further clarity on Education Planning?

Please do share your thoughts, ideas and questions on The New Age Parents Forum or you could simply drop me an email at tanooisim_winston@hotmail.com

References:

By Winston Tan, Chartered Financial Consultant

This article was first published in The New Age Parents e-magazine

Financial Planning For Your Family Series:

Part 1: Financial Priorities For Your Child

Part 2: Hospitalisation and Surgical Insurance

Part 3: Protecting The Golden Goose or Golden Egg?

Part 5: Personal Accident Plans

Part 6: Planning For Your Retirement

* * * * *

Looking to reach over 100,000 parents in Singapore? Let us amplify your message! Drop your contact details here, and we’ll reach out to you.

Discover exciting family-friendly events and places to explore! Join our Telegram channel for curated parenting recommendations.