Do you have any questions regarding financial planning or insurance questions? Do send your questions to us. Our financial experts will help you answer them.

As much as we’d like to have our life turn out according to our wish, many things are beyond our control and could impact our lives adversely.

It could be an unexpected situation like losing your belongings on an overseas trip which could ruin your travel experience; or worse, an accident which robs you of your ability to support yourself.

As the future of our health and wealth becomes increasingly uncertain, this article by PhillipCapital aims to guide you through how you can better prepare for future crises to protect your loved ones.

What can I do to prepare for an unexpected crisis?

Regardless of the crisis we face in our lives, be it death, disability or illness, or major world events that may hurt our livelihood, it pays to be prepared in advance.

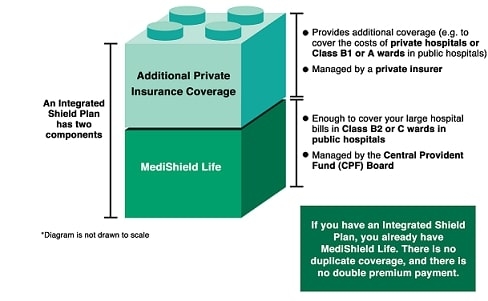

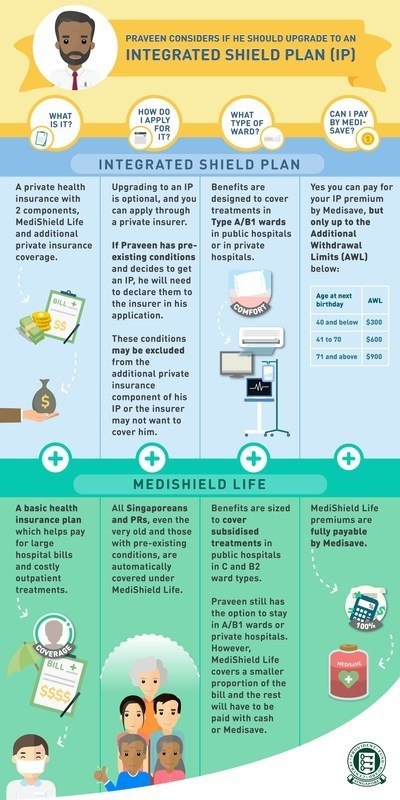

It is nobody’s wish to need hospital care but in the event this happens, do you have hospitalisation insurance that adequately covers your hospital bills? Medishield Life is just the basic cover, but it DOES NOT cover the full amount of hospital bills.

What if your hospital stay chalks up high bills due to unexpected events such as medical complications that involve intensive care, long-term hospitalisation and expensive treatments?

Will you be able to pay the bills, or worse, be forced to forgo treatment for yourself or your loved ones because of your financial difficulties? Having a good hospitalisation insurance plan could make a difference.

Source: areyouready.sg

Unexpected events such as death, disability and critical illness can cause our lives and finances to go into a tailspin. Instead of fretting over these issues, why not invest in insurance and nip your financial concerns in the bud before it starts?

Prevention (of financial headaches) is better than the cure. Purchasing affordable term insurance or investing in limited payment insurance (where you choose to only pay for a short term like 10, 15 or 20 years and be covered until old age), could save you a lot of headache in the future.

For limited payment insurance, the earlier you purchase, the more affordable it is, especially for young children. Some insurance plans also allow you to multiply your coverage affordably, for example, a 3X multiplier allows you to increase critical illness coverage by 3X until a certain age, without having to pay 3X more premiums.

What if I get into a serious accident or illness?

No matter how cautious we try to be, some accidents are beyond our control, and though we can never predict them, we can make plans to cushion the financial consequences.

Having Personal Accident insurance that covers for loss of limbs and total permanent disability provides a financial safety net for the insured. Some Personal Accident plans also allow you to claim for temporary total disablement, which will cover you if you’re unable to work temporarily due to the accident.

Serious accidents and illnesses may also cause people to lose their jobs if they are not able to work due to the injury or illness, hence having additional disability income insurance protects you against the loss of income if you are unable to work.

How can I retire without worrying about money?

We have worked hard our whole lives. Wouldn’t we want a comfortable retirement where we can afford the best things in life?

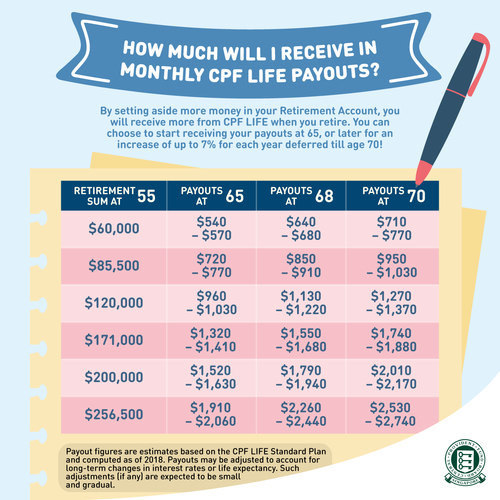

The first financial insurance plan that many people associate with retirement is CPF Life, yet CPF Life should not be the one and only retirement plan you have.

Source: areyouready.sg

Retirement plans pay out a regular income (monthly or annually) from your desired retirement age. The amount you need for retirement depends on your needs.

Having CPF Life sets a foundation for your retirement income. To better safeguard your interests in the event of unexpected life crises, other insurance plans for hospitalisation, disability and critical illness to buffer your savings should come into place.

If you are able to set aside a little bit more, consider another retirement plan or annuity to complement CPF Life. With compound interest, what you put in today will bear fruit decades later when you retire.

What should I do next to plan for crises?

Start making plans today.

Remember that prevention is always better than cure. Focus on your health and those of your loved ones.

Instead of panicking when a crisis occurs, find a trusted advisor who can help you assess your needs at different life stages and support your life goals. Reach out to PhillipCapital to draw up a financial plan to suit your needs.

Being a parent comes with added responsibilities. Besides needing to care for our spouse, parents and parents-in-law, we also need to care for our little one’s physical, emotional and social needs from the moment they are born.

To do all of the above to the best of our abilities, we need to be financially responsible and savvy.

Why Invest?

Generally, investments help you to potentially reap better returns than having your savings sit in a bank. However, investments come with risks and we need to equip ourselves with adequate knowledge before we start investing.

Here are some important investment facts to know before you start investing.

#1 Why should you start investing early and regularly?

The ultimate goal of early and regular investing is to build savings. Regular investing encourages disciplined saving and helps you to be more aware of your spending habits. Although regular investments could avail capital gains, one should be mindful not to invest blindly as every investment comes with risks.

Despite the risks involved in investments, many continue to invest regularly as the potential gains may outweigh the risks. As such, the world’s richest people continue to grow their wealth through regular investments. Many working professionals in Singapore also appreciate the benefits of early and regular investments.

#2 How Much Should You Set Aside For Investments?

Before you start investing, ask yourself these questions:

What are your financial objectives? (e.g. to save for your child’s education)

What is a comfortable figure you can set aside?

Managing finances is not an easy task, and even more challenging for the “sandwich generation” given the demands of meeting the financial needs of both your children and ageing parents. The rising childcare costs also add on to the financial stress. For example, the cost of University Education is set to rise to approximately S$180,000 by 2035.

As such, it would be ideal if your investments could be converted into cash without incurring significant fees or penalties that would reduce your overall returns.

While there is no right proportion of your income you should set aside for investments, allocating 15% to 20% of your gross income could be a safe start for beginners. There are regular fixed dollar investments plans available where you can invest from as low as $100. You may consider increasing your investments to generate higher returns as your earnings increase with career progression over the years.

#3 Should I Invest In One Fund Or Invest In A Few?

For those who are new to investing, decisions on what funds to invest in don’t come easy. Generally, it is good to diversify your investments. Diversification is a strategy for reducing risks by allocating investments in a variety of financial products with exposure to different industries and geographical locations.

This maximises returns by spreading risks across different segments so that no single event (e.g. natural disaster, change in government policy) can have a substantial impact on your returns.

An example of diversified investment is to invest in an index that has a variety of quality stocks within. For example, the Phillip SING Income ETF holds 30 high-quality SGX-listed stocks based on business quality, financial health and dividend yield.

How Long Should I Invest Before Withdrawing My Money?

This depends on your investment objectives and time horizon. It is highly recommended to invest long-term for potentially higher returns.

Time to Invest: Think Big, Start Small

You can start by taking small simple steps; begin with mindful spending and/or saving a sum of money every month. It is never too late to make the change today.

Investing is a means to grow your savings so that you can achieve your financial goals, be it for your children’s education, getting a home upgrade, or for your own retirement.

Looking for a less risky/conservative investment with a low monthly cost? A Regular Savings Plan can potentially help you reach your goals.

Benefits of Regular Savings Plans

What this means

Great for people who are new to investing

Offers consistent and disciplined means of investment. Start small from as low as $100 per month

Able to invest in equities (stocks) and Unit Trusts

39 stock counters and more than 500 funds available

Dollar cost-averaging

Does not require you to time/keep track of the volatile market

No lock-in period

Gives you flexibility, you’re able to withdraw your investment anytime

Dividend reinvestment

Allows compounding interest from your dividends to work in your favour

Hassle-free GIRO arrangement

No manual payment required

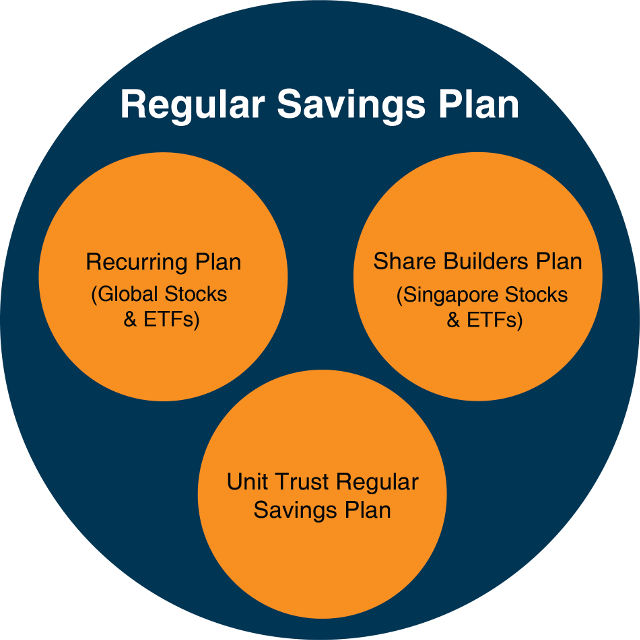

PhillipCapital offers a Regular Savings Plan that is ideal for new or budding investors. It consists of three components – Share Builders Plan, Unit Trusts Regular Savings Plan and Recurring Plan.

Source: PhillipCapital

Share Builders Plan offers flexibility by allowing you to amend your monthly investment amount to cater for unforeseen situations. It allows you to suspend your plan temporarily, till you are ready to resume.

Unit Trust Regular Savings Plan aims to turn market fluctuations to your benefit by investing a fixed amount of funds consistently every month over a period of time. By doing so, you reap the benefits of dollar-cost averaging, regardless of price fluctuations. You purchase more units when the price is lower and fewer units when the price is higher.

Recurring Plan gives you more control over your investments. Based on the Dollar Cost Averaging concept, you gradually build your portfolio over a period of time by choosing from the entire pool of Stocks and ETFs in the US, Hong Kong and Singapore market for the Recurring Plan! Additionally, you get to choose your own interval – daily, weekly, monthly or quarterly – giving you greater flexibility.

I’m Ready To Start My Investment Journey! What’s Next?

Start investing with Regular Savings Plan by opening a POEMS account in 5 minutes with MyInfo. Visit poems.com.sg/dl (mobile only) to download the app for free.

Receive up to $100* bonus credits when you sign up for Share Builders Plan

Give your child an investment head start in life! Open a Junior Share Builders Plan for your child (below 18 years of age) today!

Junior Share Builders Plan Promo: From now from till 31 December 2019, you enjoy 12 months handling fee rebates* when you sign up for Junior Share Builders Plan. For more info, visit poems.com.sg/rsp/#promo

Giveaway")

")